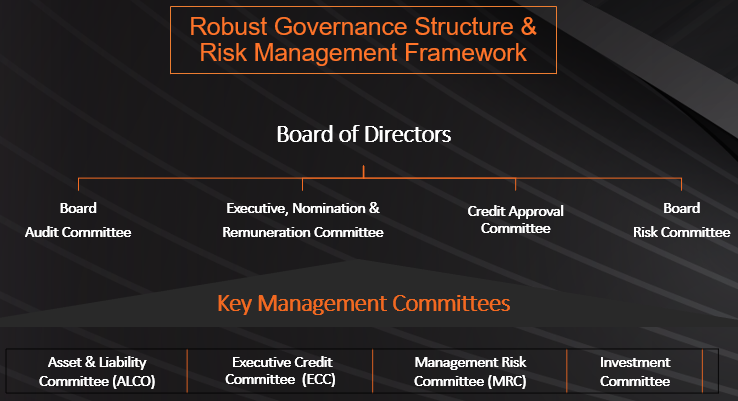

Board of Directors

The Bank’s Board of Directors (the “Board”) is the highest governing authority within the Bank’s structure. Its role is to ensure that the Bank conducts itself in accordance with its core values and develops them further on a continuous and sustainable basis. The Board consists of professionals from various fields and professions and gives representation to the stakeholders and administrators in the decision-making process. The Board composition includes 6 independent directors, out of 7, which represents a percentage of 85 percent independent directors. This structure enables meaningful discussions and an unbiased and qualitative view on matters placed before it.

There is a clear segregation between the ownership of the Bank and management. The role of the Chairman of the Board, and that of the Chief Executive Officer (“CEO”) are separated, with clear separation of responsibilities between the running of the Board, and executive management’s responsibilities in terms of running the Bank’s operations. As per applicable regulations, the CEO is prohibited from holding a Board role. The Board is responsible for overseeing how management serves the long-term interests of shareholders and other key stakeholders.

Board of Directors’ Executive Powers

- Vested with the powers of general superintendence, direction and management of the affairs and business of the Bank.

- Ultimate responsibility for the overall compliance and oversight of the management of the Bank.

- Guides the Bank to achieve its objectives in a prudent and efficient manner.

- Primarily responsible for ensuring that all financial transactions are legal and that all disclosures are made as per regulations.

- Lays down a comprehensive Code of Professional Conduct for all Board Members and Senior Management of the Bank, to be followed under all circumstances.

- Approves the delegation of power to the executive management as well as nominee members of the sub-committees and specify their roles, responsibilities and power.

- Authorizes management to implement the strategy for the Bank that is designed to deliver increasing value to the shareholders.

- Develop strategies for managing risks associated with the business and for meeting challenges posed by competitors.

- Develop a vision to anticipate crisis and to act proactively when necessary.

- Ensures that information flows upward and that authority flows downward, and therefore ensures the Bank is under their control, direction and superintendence.

Board SUB-Committees

1. Executive Nomination and Remuneration Committee (ENRC)

The ENRC assists the Board in discharging its responsibilities in relation to:

- General performance aspects of the Bank such as strategy setting and implementation, annual budget recommendations, information technology, information security, and management of environment, social, and governance (ESG) activities.

- Assists the Board in reviewing business proposals, other than credit, and other related issues that require a detailed study and analysis.

- Human Resource, Nomination, and Remuneration-related issues including providing direction and guidance in the selection and performance management of the CEO and Senior Management.

- Providing support and direction to the Board in ensuring all stakeholder interests are protected.

2. Board Audit Committee (BAC)

The main functions of BAC include:

- Assessment and review of the Bank’s financial reporting system to ensure that the financial statements are correct, sufficient, and credible.

- Review, with management, the quarterly and annual financial statements before their submission to the Board for adoption.

- Reviews the adequacy of regulatory compliance, regulatory reporting, internal control systems, and the structure of the Internal Audit and Compliance Departments. In this regard, the Committee holds discussions with the internal auditors/external auditors on significant findings regarding the control environment.

- Oversight in the discharge of the responsibilities of the Chief Internal Auditor. The role of Chief Internal Auditor is to provide assurance that the management control framework used within the Bank is operating effectively. The Chief Internal Auditor reports directly to BAC.

3. Credit Approval Committee (CAC)

The CAC assists the Board in discharging its responsibilities in relation to:

- Approval of credit and loan facilities above the credit and lending mandates of the Executive Credit Committee (ECC).

- Review of credit product policies, credit policy, credit portfolio, and existing credit facilities – all within its authority as defined under the Bank’s Wholesale Banking Credit Policy and Consumer/Retail Lending Policy.

- Review of strategies to support the Bank’s credit and lending goals and make appropriate recommendations to the Board.

- Reviews the Bank’s internal control procedures in relation to credit risk assets and ensures that they are sufficient to safeguard the quality of the Bank’s risk assets.

- Ensures compliance with regulatory requirements regarding the granting of credit facilities.

- Reviews the Bank’s Asset and Liability Management approach to ensure it is fit for purpose and in line with regulatory requirements.

- Handling issues referred to the Committee from time to time by the Board.

4. Board Risk Committee (BRC)

The Board Risk Committee (BRC) assists the Board in discharging its responsibilities in its oversight and governance in relation to the risk performance of the Bank. Responsibilities of the BRC include:

- Making recommendations to the Board on the Bank’s risk appetite in relation to credit, interest rate, market, liquidity, and operational risk.

- Oversees the implementation of the Bank’s risk strategy and policy in addition to ensuring that a robust risk framework is in place within the Bank which optimizes the quality and return on deployment of assets.

- Provides guidance and direction on all credit, market, interest rate, liquidity, and operational risk policy matters.

- The BRC also has oversight in the discharge of the responsibilities of the Chief Compliance Officer. The role of the Chief Compliance Officer is to ensure that the Bank complies with all the laws, rules and regulations as applicable under the regulatory framework in the Sultanate of Oman, other geographies in which the Bank operates and in alignment with international best practice. The Chief Compliance Officer reports directly to the BRC.

Key Management Committees

1. Executive Credit Committee (ECC)

The main responsibility of the ECC is to approve credit facilities and take credit-related decisions within the delegated authority mandated in the Bank’s Wholesale Banking Credit Policy and Consumer/Retail Lending Policy. The ECC is responsible for the following as it relates to lending matters across all the Bank’s operations:

- Approving Authority

- Oversight Function

- Governing Body

The ECC evaluates the overall risks faced by the Bank and determines the acceptable level of risks, ensuring the management and control of such risks align with the best interests of the Bank, and are in line with the Bank’s Strategy and Risk Appetite.

2. Management Risk Committee (MRC)

The MRC is primarily responsible for the oversight, implementation, and adherence to the Bank’s overarching Risk Management Framework. The MRC acts in line with the Bank’s governance structure and follows directions from the BRC. Key responsibilities of the MRC include:

- Ensures appropriate identification, assessment, measurement, mitigation, reporting, and monitoring of all non-financial risks across the Bank’s activities, including:

- Operational Risk

- Information Security Risk

- Business Continuity

- Compliance

- AML

- Financial Crime

- Legal

- Environment Social and Governance (ESG) risk

- Ensures appropriate coverage (granularity) and suitable management actions are undertaken by responsible parties in relation to control deficiencies or insufficiencies.

- Monitors non-financial risks and controls at the management level to an acceptable standard to support appropriate decision-making and enhance organizational resilience and sustainability.

- Serves as the platform where Business, Support, and Control functions present their high-rated risks, challenges, and impediments. The Committee takes the required decisions for mitigating these risks.

- Endorses policies and frameworks and directs actions to enhance the overarching control framework or risk management practices in specific areas. Risk issues and critical matters are escalated to the BRC for advice and information, as necessary.

- Establishes and enhances risk awareness and promotes a risk culture.

- Monitors, strengthens, and enhances the Bank’s Risk Management Framework and Corporate Governance in areas such as information security, legal, compliance, AML, financial crime, and ESG.

- Provides continuous guidance and oversight.

- Approves and endorses any matters pertaining to risk identification, risk monitoring, and risk controls across the Bank, as required.

- Reviews and recommends to the Board Sub-Committees bank-wide policies, risk appetite, charters, frameworks, and delegation of authorities for review, concurrence, and approval.

- Provides concurrence to key risk acceptances, including waivers and deviations presented by respective Business, Support, and Control functions.

- Reviews and monitors all activities relating to sustainability/ESG-related risks, including climate risk.

It is noted that ‘Strategic Risk’ is managed separately, outside the MRC, through appropriate senior management forums or committees. Reputational Risk is considered a sub-set of other Principal Risk types and has a secondary effect. Effective mitigation and monitoring of all non-financial risk types contribute towards sound management of Reputational Risk in the Bank.

The MRC’s scope does not cover financial risk (i.e., credit, market, and liquidity risk). These risks are critical to the Bank and are managed by the ECC, CAC, and ALCO.

3. Investment Committee

- Oversee the implementation of the Investment Policy.

- Approve investment proposals brought by the Asset Management Department and the Investment Officer.

- Recommend other policies related to investment management.

- Approve investment manager agreements and authorize execution of such agreements.

- Approve the Bank's securities lending policy.

- Monitor risk and performance on a monthly basis of investments against the Bank’s agreed investment objectives.

- Review monitoring reports provided by the Investment Division.

- Review performance of Asset Management Department and take remedial action where necessary.

4. Asset and Liability Committee (ALCO)

The Bank’s Asset and Liability Committee (ALCO) is dedicated to managing and optimizing the Bank's balance sheet, ensuring effective liquidity management, and mitigating financial risks. Key responsibilities include:

- Ensuring adequate liquidity to meet the Bank's obligations and strategic requirements.

- Monitoring and managing the Bank's exposure to fluctuations in interest rates and broader interest rate risk management activities.

- Strategically aligning assets and liabilities to enhance financial performance and stability and optimizing the Bank’s balance sheet.

- Ensuring the Bank maintains sufficient capital to support its operations and growth.

- Adhering to regulatory requirements and industry standards for financial management.

Other Management Committees

1. Model Governance Committee (MGC)

The MGC is a sub-committee of the MRC. This Committee supersedes the IFRS 9 Steering Committee. The MGC's scope and mandate have been expanded to include model governance in relation to IFRS 9 Expected Credit Loss (ECL) Models, ICAAP Models, Stress Testing Models, Rating/Scoring Models, and other financial risk models (e.g., Revenue Sharing, Cost Allocation, Risk Appetite, FTP), as delegated by the MRC.

- Oversight of the reliability and performance of the Bank’s financial risk models.

- Provide confidence in the functional and operational effectiveness of the Bank’s models.

- Ensure the Bank’s models are periodically reviewed to ensure accuracy and reliability of predicted values.

- Approve the appointment of advisors and/or consultants in relation to model governance for areas such as review, validation, upgrades, modifications, enhancements, and integrations.

- Endorse the results of reviews, amendments, enhancements, and other requirements of the Bank’s models, referring to the MRC for approval.

2. Special Asset Management Credit Committee (SAMCC)

The SAMCC is responsible for reviewing the performance of the special asset portfolio, including stressed assets, remedial department assets, and other assets/loans requiring updates or decisions.

The SAMCC is a sub-committee of the MRC. Within its delegation, responsibilities include:

- Periodic review of the special asset credit portfolio.

- Review and provide recommendations to the MRC on credit/write-off proposals for qualifying non-performing assets across different portfolio segments.

- Review key performance indicators and monitoring reports of the Bank’s stressed assets portfolio.

- Approve and review any other general items within the Committee’s delegation.

3. Business Technology Committee (BTC)

The BTC focuses on oversight and management of the Bank’s technology and digital initiatives. Its responsibilities include:

- Providing strategic direction and ensuring technology initiatives align with the overall business strategy and goals of the organization.

- Tracking the performance of technology systems, projects, and initiatives to ensure they deliver value and meet predefined objectives.

- Ensuring technology policies, practices, and systems comply with legal, regulatory, and industry standards, maintaining strong governance of technology projects.

- Overseeing project implementation and supporting the prioritization of projects in alignment with the Bank’s strategic objectives, regulatory requirements/changes, and market changes.